I. Introduction to Our Company and Crowdfunding

GigaStar Portal LLC (“Funding Portal” or "GigaStar Market") is an SEC registered Funding Portal and member of FINRA, which offers securities under Regulations Crowdfunding (Title III Crowdfunding) to investors 18 or older. Investments made through GigaStar Portal LLC are speculative, illiquid, and involve a high degree of risk, including the possible loss of your entire investment.

Crowdfunding is a new and evolving method for individuals and small companies looking to raise capital using the internet. Companies and individuals employing crowdfunding are usually looking to raise smaller amounts of capital from a larger group of investors. This is contrary to the more traditional model where small companies focus on a single financier or small group of investors to provide “seed” or “start-up capital.”

The Securities and Exchange Commission (“SEC”) adopted rules to permit companies to offer and sell securities through crowdfunding in reliance on the exemption under Section 4(a)(6) of the Securities Act of 1933 (“Securities Act”). These new rules implement the requirements of Title III of the Jumpstart Our Business Startup (“JOBS”) Act, which added Sections 4(a)(6) and 4A to the Securities Act and Sections 3(h) and 12(g)(6) to the Securities Exchange Act of 1934 (“Exchange Act”). A “funding portal” is a Title III crowdfunding intermediary that, in accordance with Section 304(b) of the JOBS Act and Exchange Act Section 3(a)(80), can engage in specifically enumerated crowdfunding activities.

II. Our Funding Portal and Process

We are a Funding Portal that is registered with SEC and a member of FINRA. We are not a broker-dealer or an investment advisor. Funding Portals are a virtual internet-based marketplace (i.e., an intermediary) that connects companies that wish to raise capital through securities offerings with individuals who are seeking investment opportunities. As a Funding Portal, we cannot and will not:

- Offer investment advice or recommendations;

- Solicit purchases, sales or offers to buy the securities offered on our platform;

- Compensate employees, agents, investors, or entities seeking investment capital other persons for such solicitation or based on the sale of securities displayed or referenced on our funding portal; or

- Hold, manage, or handle in any manner investor funds or securities.

We create business relationships with companies that wish to raise capital (i.e., “issuers”) who pay us for access to our funding portal. Our relationship with an issuer may be related to a one-time securities offering or for multiple securities offerings over a longer period of time. Following completion of an offering, there may or may not be any ongoing relationship between the issuer and the funding portal.

We may receive compensation from issuers in the form of payment (e.g., monies or securities) as a percentage of funds raised on our funding portal, a flat fee, or in other ways. Investors may refer to the issuer’s respective offering documentation (e.g., Form C) that is found on our portal and the SEC’s EDGAR website (https://www.sec.gov/edgar/searchedgar/companysearch.html) for additional information.

B. Types of Securities Displayed and Associated Risks

The securities offerings listed on our portal are private securities offerings, which are also known as “non-public offerings”. These offerings are not publicly listed on an Exchange (e.g., New York Stock Exchange) and are not assigned a CUSIP. As a private offering, the securities listed on our platform are subject to risks, including the risk of loss of principal and there may not be a secondary market to sell the securities.

The securities displayed on our Funding Portal include the following types of securities:

Revenue Sharing Securities (e.g., Revenue Sharing Units): Revenue sharing securities are issued in units and offer investors a percentage of an Issuer’s potential future revenues. When you buy a revenue sharing security, you are not an equity owner nor a creditor to the issuer. The terms of each revenue sharing security should be read carefully to understand how much of the issuer’s future revenues you are entitled to and for how long in time the agreement lasts.

These securities are highly speculative and involve are substantial risks including, but not limited to the following:

- Possible loss of entire investment;

- Possibility of not future revenue or return of investment;

- Liquidity risk as the securities are not able to be sold for 12 months after the offering closes and there may not be an active secondary market thereafter.

Please also see the General Funding Portal Offering Risks section below for additional risks related to securities offerings. Please also review and understand Form C that details the risks associated with these offering prior to investing.

Channel Revenue Tokens (CRTs): Channel Revenue Tokens are a cryptographic tool which represents the underlying asset in digital form. The CRT is created (or ‘minted’) and recorded using blockchain technology after the Reg CF offering closes CRTs use blockchain technology to establish authenticity, ownership, and transferability of the unique Revenue Sharing Security unit that was issued through the Reg CF offering.

Tokens are a form of technology that also involve risks including, but not limited to the following:

- Underlying Loss or Damage of Physical Asset;

- Blockchain & Smart Contract Transactions and Cybersecurity;

- Evolving Regulatory Framework

Please see the “Token Related Risk Considerations” discussion in the subsequent “General Funding Portal Offering Risks” section below for explanations of general risks related to tokens.

Token Related Service Providers: Potential investors are advised that the GigaStar Portal LLC is not involved with the tokenization or blockchain processes, which occur after the closing of a Reg CF offering. Channel Revenue Tokens are minted and added to the blockchain by GigaStar Technologies LLC. GigaStar Technologies LLC is an affiliated company of GigaStar Portal LLC, but GigaStar Technologies LLC is not a member of FINRA nor is it registered with the SEC.

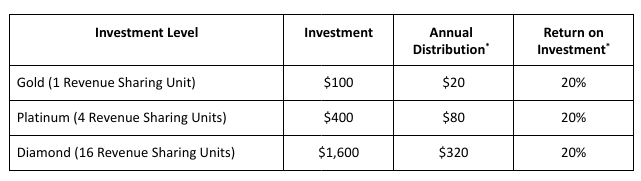

Hypothetical Illustration: For this hypothetical illustration of the potential shared revenue that would be distributed to the Revenue Sharing Units (digitally represented by CRTs) from a Reg CF offering, assume the following terms applied to a one-year period after the closing of the Reg CF offering:- Offering Terms:

The Reg CF offering contains the following terms:

a. Annual Revenue Sharing Percentage of Channel’s YouTube Revenue: 40%

b. Minimum Target Offering Amount: $200,000

c. Number of Revenue Sharing Units Issued: 2,000

d. Price per Unit: $100

- Reg CF Offering Closing Results:

The Offering successfully sells 2,000 Revenue Sharing Units raising $200,000 for the Issuer.

- Channel’s Annual Revenue:

One year after the Reg CF offering, the Channel's YouTube Revenue for the one-year period after the closing is: $100,000.

- Total Annual Revenue Share:

Pursuant to the Offering Terms, the total 2,000 Units will receive 40% of the Channel's YouTube Revenue for the current one-year

period, which is: $40,000.

(Math: $100,000 YouTube Revenue x 40% revenue sharing = $40,000)

- Annual Revenue Sharing Distribution to Units:

Each Unit will receive their respective Unit’s allocation of revenue share from the Channel’s YouTube Revenue for the current one-year

period, which is $20 per Unit.

(Math: $100,000 YouTube Revenue x 40% revenue sharing = $40,000 / 2000 Total Units = $20 per Unit.)

Based on the foregoing example, the respective annual revenue sharing distribution and return on a Gold, Platinum or Diamond level investment (excluding fees) would be as follows based upon*:

*This illustration is hypothetical in nature, does not reflect actual investment results, excludes fees, and is not a guarantee of future results. This illustration does not compare or illustrate any specific investment offering. Investment offerings on this platform are speculative, illiquid, and involve a high degree of risk, including the risk of loss of your entire investment.

GigaStar Markets makes no warranties or representations related to these illustrations and the applicability or accuracy regarding your individual circumstances. This hypothetical example is for illustrative purposes only and is not to be considered investment advice or an investment recommendation. Investors should consult with a qualified financial and tax advisor before investing.

Investors should refer to the respective offering documentation (e.g., Form C, etc.) found on the respective Offering Page for terms, conditions, features and associated risks with the particular security offered.

III. General Funding Portal Offering Risks

The following is a non-exhaustive list of general risks that are associated with Title III investments that may be displayed on our funding portal platform. Investors should review the issuer’s offering documentation (e.g., Form C) for additional risks specifically related to the respective offering(s) that are available for investment on the funding portal.

- Risk of Loss: The risk that the investor may not receive part, or all, of the amount invested to purchase the security. Investors should only invest money in Title III securities that they can afford to lose.

- Liquidity Risk: The risk of a lack of an active secondary market for securities purchased. Investors will not be able to sell Title III securities for the one-year resale restriction period. Further, there may not be a ready market to sell Title III securities after the restricted period is over.

- Market Risk: The possibility for an investor to experience losses due to factors that affect the overall performance of the financial markets in which the investor is involved.

- Performance Risk: It is not possible to predict the performance of a company based upon its past performance. Past performance is not indicative of future results and there can be no assurance that targeted results will be achieved. Loss of all, or a portion of, your principal is possible, and even likely, on any given investment.

- Dilution Risk: The risk that the issuing company may issue additional equity securities in the future, which will result in the percentage of ownership that the investor previously held will be lower after the additional issuance of equity. Additionally, there is a risk of having limited voting power as a result of dilution after subsequent equity with voting rights has been issued.

- Inflation Risk: The risk that the purchasing power of the investment asset does not keep pace with the purchasing power of another asset such as the currency used to initially purchase the investment asset.

- Interest Rate Risk: The risk that arises for bond owners from fluctuating interest rates. How much interest rate risk inherent in a bond depends on how sensitive its price is to interest rate changes in the market. The bond’s sensitivity depends on two things, the bond's time to maturity, and the coupon rate of the bond.

- Credit Risk / Default Risk: This is the risk associated with whether the Issuer of the security will continue to be able to pay its debt, including any stated interest rate to the investor.

- Token Related Risk Considerations: In addition to the Token risk considerations specific to the offering detailed in the Issuer’s respective Form C, the following risk consideration generally apply to Tokens.

- Blockchain Transactions and Cybersecurity: Transactions on the blockchain are generally anonymous and irreversible. Investors must safeguard their blockchain credentials.

- Smart Contacts: Blockchain and smart contracts are interconnected. A smart contract is a digital representation of real-world agreements or contracts. The vulnerabilities in smart contact security are dependent upon the computer code or software on which it operates.

- Risk of Fraud: Although the blockchain technology is intended to create an audit trail of ownership, the risk of fraud persists which is in part due to the anonymity of blockchain technology. There are a number of other ways a fraudster could commit fraud, including but not limited to falsely claiming copyrights, royalty rights, trademarks, etc.

- Evolving Regulatory Framework: Tokens are a relatively new asset class and subject to the potential for changes in legal and regulatory framework.

- Evaluation in Secondary Market: The valuation of a Token depends upon scarcity and the perception of owners and buyers alongside the availability of distribution channels. It may be difficult to anticipate the identity of the next buyer of a Token or the possible factors which can drive their purchase. Beware of fake Token s as well as Token related scams in the secondary market.

- Intellectual Property Rights: When evaluating whether to purchase a Token, it is important to validate that the seller owns the Token. There have been examples of people selling photos of Tokens or minting Token replicas.

- Liquidity: In addition to Reg CF illiquidity considerations, a Token may not have an activity secondary market and an investor may not be able to sell their Token. Please see Reg CF illiquidity and holding period considerations as well.

Investors are also encouraged to consult with their qualified financial and tax advisors prior to making any investment.

- SEC Investor Bulletin - Updated Investor Bulletin: Crowdfunding for Investors, May 10, 2017

The SEC issued an Investor Bulletin on February 16, 2016, which was updated on May 10, 2017, that provide general examples of some of the risks associated with Title III investments. Please see the SEC’s description below as well as the respective Investor Bulletins for additional information. These risks also apply to investments on our Funding Portal platform.

- Speculative: Investments in startups and early-stage ventures are speculative and these enterprises often fail. Unlike an investment in a mature business where there is a track record of revenue and income, the success of a startup or early-stage venture often relies on the development of a new product or service that may or may not find a market. You should be able to afford and be prepared to lose your entire investment.

- Illiquidity: You will be limited in your ability to resell your investment for the first year and may need to hold your investment for an indefinite period of time. Unlike investing in companies listed on a stock exchange where you can quickly and easily trade securities on a market, you may have to locate an interested buyer when you do seek to resell your crowdfunded investment.

- Cancellation restrictions: Once you make an investment commitment for a crowdfunding offering, you will be committed to make that investment (unless you cancel your commitment within a specified period of time). Investors have up to 48 hours prior to the end of the offer period to change your mind and cancel your investment commitment for any reason. Once the offering period is within 48 hours of ending, you will not be able to cancel for any reason even if you make your commitment during this period. However, if the company makes a material change to the offering terms or other information disclosed to you, you will be given five business days to reconfirm your investment commitment.

- Valuation and capitalization: Your crowdfunding investment may purchase an equity stake in a startup. Unlike listed companies that are valued publicly through market-driven stock prices, the valuation of private companies, especially startups, is difficult and you may risk overpaying for the equity stake you receive. In addition, there may be additional classes of equity with rights that are superior to the class of equity being sold through crowdfunding.

- Limited disclosure: The company must disclose information about the company, its business plan, the offering, and its anticipated use of proceeds, among other things. An early-stage company may be able to provide only limited information about its business plan and operations because it does not have fully developed operations or a long history to provide more disclosure. The company is also only obligated to file information annually regarding its business, including financial statements. A publicly listed company, in contrast, is required to file annual and quarterly reports and promptly disclose certain events—continuing disclosure that you can use to evaluate the status of your investment. In contrast, you may have only limited continuing disclosure about your crowdfunding investment.

- Investment in personnel: An early-stage investment is also an investment in the entrepreneur or management of the company. Being able to execute on the business plan is often an important factor in whether the business is viable and successful. You should also be aware that a portion of your investment may fund the compensation of the company’s employees, including its management. You should carefully review any disclosure regarding the company’s use of proceeds.

- Possibility of fraud: In light of the relative ease with which early-stage companies can raise funds through crowdfunding, it may be the case that certain opportunities turn out to be money-losing fraudulent schemes. As with other investments, there is no guarantee that crowdfunding investments will be immune from fraud.

- Lack of professional guidance: Many successful companies partially attribute their early success to the guidance of professional early-stage investors (e.g., angel investors and venture capital firms). These investors often negotiate for seats on the company’s board of directors and play an important role through their resources, contacts and experience in assisting early-stage companies in executing on their business plans. An early-stage company primarily financed through crowdfunding may not have the benefit of such professional investors.

Source: https://www.sec.gov/oiea/investor-alerts-bulletins/ib_crowdfunding-.html

IV. Issuance and Offering Processes

An issuer who wishes to raise capital under a Title III crowdfunding campaign may sell up to $5,000,000 million in any rolling 12-month period to individual investors.

A. Eligible Issuers

The ability to engage in crowdfunding is not available to all issuers. By statute, the following issuers cannot rely on crowdfunding transactions under Section 4(a)(6):

- issuers not organized under the laws of a state or territory of the United States or the District of Columbia;

- issuers already subject to Securities Exchange Act of 1934, as amended (the “Exchange Act”) reporting requirements;

- investment companies as defined in the Investment Company Act of 1940 (the “Investment Company Act”) or companies that are excluded from the definition of “investment company” under Section 3(b) or 3(c) of the Investment Company Act; and

- any issuer that the United States Securities and Exchange Commission (“SEC”), by rule or regulation, determines appropriate.

The final SEC rule also excludes the following issuers:

- issuers disqualified from relying on Section 4(a)(6), or “bad actors;” and

- issuers that have sold securities in reliance on Section 4(a)(6) and have failed, to the extent required, to make required ongoing reports required by Regulation Crowdfunding during the two-year period immediately preceding the filing of the required new offering statement; and

- any issuer that is a development stage company that has no specific business plan or purpose, or has indicated that its business plan is to engage in a merger or acquisition with an unidentified company or companies

We will request, and may rely upon, representations from the issuer regarding their eligibility to conduct a Title III offering on our funding portal. We will conduct certain issuer due diligence that may include the collection and review of information and documentation related to the following:

- securities enforcement regulatory history related to the issuer.

- securities enforcement regulatory history on each officer, director or beneficial owner of 20 percent or more of the issuer’s outstanding voting equity securities.

During our due diligence process, we may also collect and review information related to the company’s financial condition, business plan as well as other information and documentation that may be relevant in determining that the issuer is not disqualified under regulations from participating on our funding portal. The due diligence that our funding portal conducts is not a substitute for an investor’s own due diligence into the financial standing, investment merits or suitability of any offering on our funding portal.

C. Denying Issuer Funding Portal Access

We will deny access to our funding portal if we have a reasonable basis for believing that an issuer or any of its officers, directors or beneficial owners (as defined above) is subject to a disqualification under federal rules and regulations. We will also deny issuer’s access to our funding portal if we have reason to believe that an offering is fraudulent or otherwise raises concerns about investor protection as defined under regulations.

It is important that investors also conduct their own issuer due diligence for any given offering that they are considering, as due diligence is an important step in determining the appropriateness and merits of an investment.

D. Issuer Disqualification from Title III Offerings

A securities issuer may not participate in a Title III offering if it or any of its predecessors, directors, officers, general partners or managers have been the subject of disqualification as defined under securities regulations. Regulations also state that the issuer will be subject to disqualification if any of its beneficial owners, solicitors or promoters are subject to disqualification. Title III may not be used if the issuer or certain other people have been the subject of certain disqualifying events during the last 10 years.

Regulations provide for a list of certain events that disqualify an issuer from participation in Title III offerings. These disqualifying events generally regard criminal or fraudulent activities, such as a conviction of a felony or misdemeanor in connection with the purchase or sale of any security, or the loss of license of a securities broker for misconduct. They also regard other criminal activity, such as robbery, theft and the like.

As previously mentioned, it is important for investors to remember that we cannot make investment recommendations and we do not provide any guarantees related to the investment merits or the performance of any securities offering on our funding portal. It is up to you, the investor, to decide if an investment in any offering is appropriate and suitable for you.

E. Issuer Disclosures and Form C

Issuers are required to disclose certain information through “Form C” which is filed on the SEC’s EDGAR website and will be viewable on our funding portal. Form C includes, among other things, the following information that investors may consider when determining whether to invest in a Title III offering.

- The issuer’s name, contact information and website.

- The issuer’s directors and officers.

- The issuer’s beneficial owners.

- The issuer’s financial information and discussion of the financial condition.

- Target offering amount.

- Deadline for offering.

- A description of the issuer’s business and business plan.

- A description of how the proceeds of the offering will be used by the issuer.

- The issuer’s ownership and capital structure.

- A description of how rights exercised by the principals of the issuer could affect investors.

- The compensation paid to the funding portal for the offering.

- A description of previous securities offerings by the respective issuer.

- Whether the issuer has previously failed to file the reports required by law.

- Transactions with officers, directors, and other “insiders”.

- Whether the issuer would be disqualified from offering securities under Title III under the “bad

actor” rules. - A discussion of the issuer’s financial condition.

- How the issuer will handle over-subscriptions in the offering.

- Where and when the issuer’s annual reports will be available.

- The risk factors associated with the investment.

As mentioned, the issuers offering securities that you invest in are required to disclose a only limited amount of information to you, but the issuer is required to provide financial information to you. Regulations provide for a tiered financial disclosure requirement by the issuing company.

The financial disclosures required by issuers depends on the offerings it has engaged in during the prior 12-month period. The following is a breakdown of the current financial disclosure requirements:

- $124,000 or less – financial statements and specific line items from income tax returns, both of which are certified by the principal executive officer of the company.

- $124,000.01 to $618,000 – financial statements reviewed by an independent public accountant and the accountant’s review report.

- $618,000.01 to $1,235,000 – if first time crowdfunding, then financial statements reviewed by an independent public accountant and the accountant’s review report, otherwise financial statements audited by an independent public accountant and the accountant’s audit report.

- $1,235,000.01 to $5,000,000 - financial statements audited by an independent public accountant and the accountant’s audit report.

To determine the financial statements required under Reg CF, Rule 201, an issuer must aggregate amounts sold under Reg CF within the preceding 12-month period as well as the current offering. If the issuer will accept proceeds in excess of the target offering amount, the issuer must include the maximum offering amount that the issuer will accept in the calculation to determine the financial statements required. Issuers should refer to Rule 201.

F. Offering Amount, Deadline and Early Completion

The issuer will also disclose its “target offering amount” on Form C as well as the offering deadline that they have set to close its offering to investments. The target offering amount is the minimum amount of capital that the issuer is attempting to raise.

If the target offering amount is not reached the issuer will typically cancel the offering and the investors who made an investment commitment will receive notification of the cancellation and be returned their money.

If an issuer reaches the target offering amount prior to the deadline identified in its offering materials, the issuer may close the offering on a date earlier than the deadline identified in its offering materials provided, among other things, that the investor is provided notice of:

- The new, anticipated deadline of the offering;

- The right of investors to cancel investment commitments for any reason until 48 hours prior to the new offering deadline; and

- Whether the issuer will continue to accept investment commitments during the 48- hour period prior to the new offering deadline.

If an Issuer intends to accept investments over and above the target offering amount, it must disclose the maximum amount it will accept and how it will handle “over-subscriptions.” For example, the Issuer might allocate the securities on a first-come first-served basis, or pro-rata among all of the investors who make investment commitments, or in some other way.

G. Issuer Cancellations, Material Changes and ReconfirmationsAs detailed in the prior section, the Issuer may cancel the offering if the offering does not reach its minimum target amount by the closing date. The Issuer may also cancel the offering for any reason, as detailed in the respective Form C.

If an issuer makes a material change to the terms of an offering or the information previously provided by the issuer changes, we provide a means by which the issuer will send an electronic message to any investor who has made an investment commitment. The electronic message will describe that the investor’s investment commitment is cancelled unless the investor reconfirms their investment commitment within five (5) business days of receipt of the message.

If the investor does not reconfirm the investment commitment on the funding portal, the investment commitment will be cancelled and the investor’s funds will be returned to them.

Investors will receive a notification of the canceled investment commitment.

If there are material changes to the terms of the offering or the issuer’s disclosure information has changed within five (5) business days of the offering deadline (i.e., the closing date of the offering), the offering will be extended for (5) five additional business days so that the investor has the opportunity to reconfirm their investment commitment.

Funding Portal Cancellations

The Funding Portal may also cancel the offering if the Issuer does not meet the terms and conditions of its listing agreement.

H. Restrictions on Resale

Securities issued in accordance with Title III via our funding portal may not be transferred by any initial purchaser of such securities during the one-year period beginning when the securities were issued. There are, however, the following exceptions that allow transfer during this period if they are transferred to one of the following:

- To the issuer of the securities;

- To an accredited investor;

- As part of an offering registered with the SEC; or

- To a member of the family of the purchaser.

For purposes of Title III, the term “family member” means a child, stepchild, grandchild, parent, stepparent, grandparent, spouse or spousal equivalent, sibling, mother-in-law, father-in-law, son-in-law, daughter-in-law, brother-in-law, or sister-in-law, including adoptive relationships.

For purposes of Title III, an “accredited investor”, in the context of a natural person, includes anyone who:

- earned income that exceeded $200,000 (or $300,000 together with a spouse) in each of the prior two years, and reasonably expects the same for the current year, OR

- has a net worth over $1 million, either alone or together with a spouse (excluding the value of the person’s primary residence)

Investors should consult a qualified securities attorney regarding any questions on resales of Title III securities. Investors should note that we do not currently facilitate secondary market transactions or transfers on our funding portal.

I. Issuer Annual Reporting and Discontinuance of Annual Reporting

Issuers are generally required to file annual reports via Form C-AR with the SEC and post them on its own website within 120 days after the end of the fiscal year. The annual report will generally include:

- Some of the same information that is disclosed on Form C (i.e., the original offering document);

- Current financial statements certified by the principal executive officer; and

- Certain current disclosures about the issuer’s financial condition.

The issuer is permitted to discontinue filing annual reports at the date that one of the following occurs:

- The date the issuer filed, since its most recent sale of securities pursuant to this part, at least one annual report pursuant to this section and has fewer than 300 holders of record;

- The issuer has filed, since its most recent sale of securities pursuant to this part, the annual reports required pursuant to this section for at least the three most recent years and has total assets that do not exceed $10,000,000;

- The date the issuer or someone else buys all of the securities issued under Title III offerings;

- The date the issuer registers its securities and is required to file reports under the Securities Exchange Act of 1934; or

- The issuer liquidates or dissolves its business in accordance with state law.

The issuer must file Form C-TR with the SEC if it terminates annual reporting. As you can see, if the issuer discontinues annual reporting you will no longer have annually updated financial information or disclosure information about the issuer or your Title III securities that you own.

V. Investor Purchase Process

A. Investor Registration

To invest in an offering on our funding portal, investors must first register on our funding portal. Our entire investment process occurs via our funding portal that is found on our website and via the electronic delivery of information and documentation. In other words, we will not provide Investors with physical paper account applications, statements or other physical materials. Further, we do not have registered representatives (e.g., brokers or investment advisors) for you to call with investment questions or questions related to the functionality of the funding portal.

When you register on our website, we will ask you for certain identifying information and ask you to setup a user identification and password for the funding portal. It is very important that you remember these registration credentials to access the funding portal in the future. Please see our Privacy Policy for information regarding the safeguards we have for maintaining the confidentiality of your personal information.

Once you have registered you will be able to view and accept the terms and conditions of our “Investor Agreement” (Subscription Agreement), which you must read and understand prior to making an investment via our funding portal. Once you electronically sign the Investor Agreement you will then be able to view and make investments via our funding portal.

B. Investor Suitability Considerations

As a funding portal, we are prohibited from assisting potential investors with determining if an investment is appropriate for them. Further, as a funding portal, we are prohibited from making recommendations or providing investment advice. Accordingly, potential investors must independently determine if the offering(s) on our funding portal are appropriate for them considering their respective financial situation, need for liquidity, risk tolerance, and investment profile.

For these reasons, potential investors should consider consulting with a qualified financial and tax advisor prior to making any investment in any Title III offering.

Investors should fully understand the following prior to making any investment on our funding portal.

- Offering’s terms and conditions,

- Offering’s features and structures;

- Offering’s related fees, and;

- Offering’s respective risks.

Potential investors may refer to the respective Issuer’s Form C and offering information for specific information related to the offering.

C. Investor Investment Limitations - § 227.100(a)(2)

Individual investors have an aggregate limit that applies to all Title investments made by the individual over a 12-month period in all crowdfunded offerings. Remember that this individual limit is aggregate to all Title III offering across all funding portals that an individual may participate on in the rolling 12- month period from the date preceding each transaction.

Where the purchaser is not an accredited investor (as defined in Rule 501 of Regulation D), the aggregate amount of securities sold to such an investor across all issuers in reliance on section 4(a)(6) of the Securities Act (15 U.S.C. 77d(a)(6)) during the 12-month period preceding the date of such transaction, including the securities sold to such investor in such transaction, shall not exceed:

- The greater of $2,500, or 5 percent of the greater of the investor's annual income or net worth, if either the investor's annual income or net worth is less than $124,000; or

- Ten percent (10%) of the greater of the investor's annual income or net worth, not to exceed an amount sold of $124,000, if both the investor's annual income and net worth are equal to or more than $124,000;

These limits apply to everyone except “accredited investors". For accredited investors, this limit has been removed and an accredited investor may invest up to any maximum amount set in the offering documents.

To calculating you net worth you simply add your assets and subtract your liabilities. The result is your net worth. Please note that for purposes of determining eligibility in crowdfunding offerings, the value of your primary residence is not included in your net worth calculation.

In addition, any mortgage or other loan on your home does not count as a liability up to the fair market value of your home. If the loan is for more than the fair market value of your home (i.e., if your mortgage is underwater), then the loan amount that is over the fair market value counts as a liability under the net worth test.

Further, any increase in the loan amount in the 60 days prior to your purchase of the securities (even if the loan amount doesn’t exceed the value of the residence) will count as a liability as well. The reason for this is to prevent net worth from being artificially inflated through converting home equity into cash or other assets.

D. Notice of Investment Commitment

Once you decide to make an investment in an offering displayed on the funding portal and make an investment commitment, we will send you an electronic message notifying you of the following:

- The dollar amount of your investment commitment;

- The price of the securities, if known;

- The name of the issuer; and

- The date and time by which you may cancel your investment commitment.

Pursuant to regulations, an investor may cancel an investment commitment for any reason until 48 hours prior to the deadline identified in the issuer’s respective offering materials (i.e. via Form C). Investors may process such a cancellation via the funding portal by logging into their investor profile.

If the issuer announces a “material” change (i.e., a material changes information that may affect your investment decision) in the offering after you make your investment commitment, then your commitment will automatically be canceled. As previously described, you will receive notification of this change and be asked to reconfirm your investment commitment.

F. Investment Payments

Once you have selected an investment, you may pay for the investment using the features on the website, which may allow you to wire payment, ACH transfer, or check by mail. Your funds will be held at a qualified third-party financial institution as detailed under Regulation Crowdfunding, such as an escrow agent. Remember that we are prohibited from holding or maintaining your funds.

G. Confirmations of Transactions

We will at, or before, the completion of a transaction, notify investors of the following:

- The date of the transaction;

- The type of security that the investor is purchasing;

- The identity, price, and number of securities purchased by the investor, as well as the number of securities sold by the issuer in the transaction and the price(s) at which the securities were sold;

- If a debt security, the interest rate and the yield to maturity calculated from the price paid and the maturity date;

- If a callable security, the first date that the security can be called by the issuer; and

- The source, form and amount of any remuneration received or to be received by the intermediary in connection with the transaction, including any remuneration received or to be received by the intermediary from persons other than the issuer.

A promoter is a third-party hired by an issuer of Title III securities who discusses (i.e., promotes) an issuer’s offerings via a chatroom or other communication channel. The person promoting the offering must identify themselves as a “promoter” when engaging in promotional activities. The promoter must disclose their compensation for engaging in promoting a Title III offering. Investors may see “promoters'' in the chatrooms on our funding portal.

I. Communication Channels

As mentioned, we facilitate an online “chatroom” or “communication channel” on our funding portal where investors and issuers may communicate. Our chatroom is open to the public, but only investors that have registered on our funding portal may participate in the chatrooms. As mentioned, “promoters” are identified in our chatrooms.